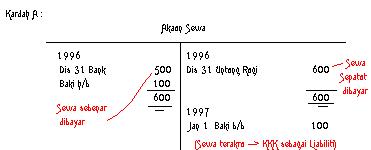

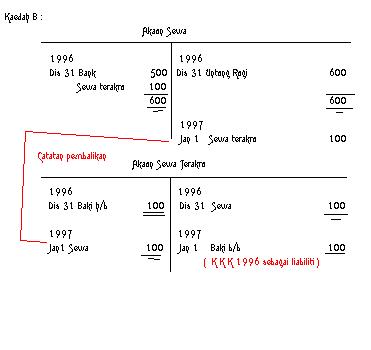

1. Belanja terakru/ terhutang/ tertunggak / belum bayat

contoh : sewa dibayar

RM 500 dengan cek

sewa bulanan RM 50

Catatan Jurnal

Dt Kt

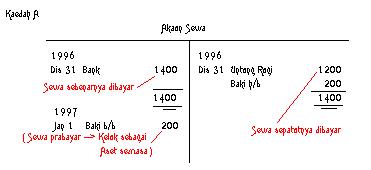

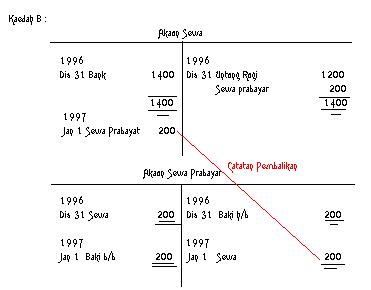

2. Belanja Prabayar / bayar terdahulu

contoh : Imbangan

Duga menunjukkan baki sewa

Dt RM 1400

( Sewa tahunan RM 1200 )

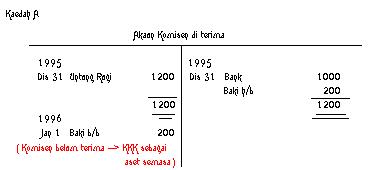

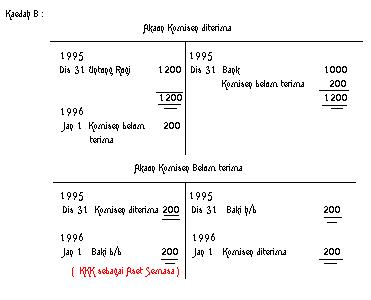

3. Hasil / pendapatan terakru/ terhutang /belum terima

contoh : Imbangan Duga

menunjukkan baki kt akaun komisen diterima

RM 1000. Komisen patut di terima RM 1200

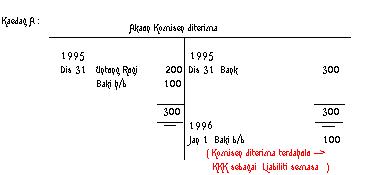

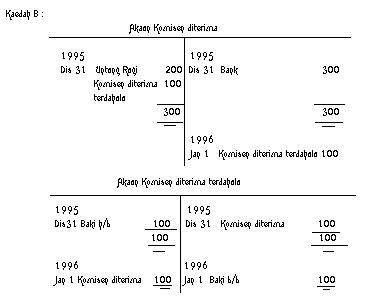

4. Hasil / pendapatan diterima terdahulu

contoh : Komisen telah

diterima RM 300

Komisen patut diterma RM 200

Catatan Juranal

Dt Kt

Kesimpulan :

Catatan Jurnal

Dt Kt

Jenis-jenis modal

1. Modal terlabur - > modal yang dilaburkan

-> tidak dicampur untung atau ditolak rugi atau ambilan

2. Modal digunakan -> Jumlah Aset - Jumlah Liabiliti = modal

akhir

( "aset bersih" jika pemilik tunggal )

3. Modal Kerja -> Jumlah aset semasa

- jumlah liabiliti semasa